Changes to the Federal Housing Finance Agency’s mortgage pricing are creating a stir in the marketplace, not that the bureaucracy wants to admit it. The changes, which took effect Monday, raise costs for some good-credit borrowers while making mortgages cheaper for low-income borrowers.

We highlighted the changes in a recent editorial, and FHFA Director Sandra Thompson objected to our characterization that the plan will socialize mortgage-lending risk. Ms. Thompson says the new policy “won’t impose higher fees on higher-credit-score borrowers than on lower-credit-score borrowers, all else equal.” She says some borrowers with higher credit scores may even pay less.

kAm(6 H@?56C 9@H D96 567:?6D “2== 6=D6 6BF2=]” %96 ?6H CF=6D 255 766D 7@C >2?J 3@CC@H6CD H:E9 9:89 4C65:E C2E:?8D 2?5 =2C86 5@H? A2J>6?ED 2?5 FD6 E96> E@ C65F46 E96 4@DE @7 3@CC@H:?8 7@C E9@D6 H:E9 H@CD6 4C65:E 2?5 D>2==6C 5@H? A2J>6?ED]k^Am

GALLERY: Editorial cartoons for May 2023

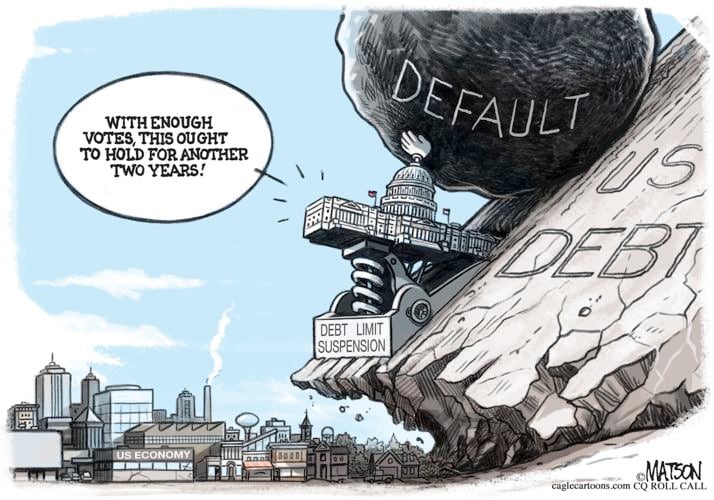

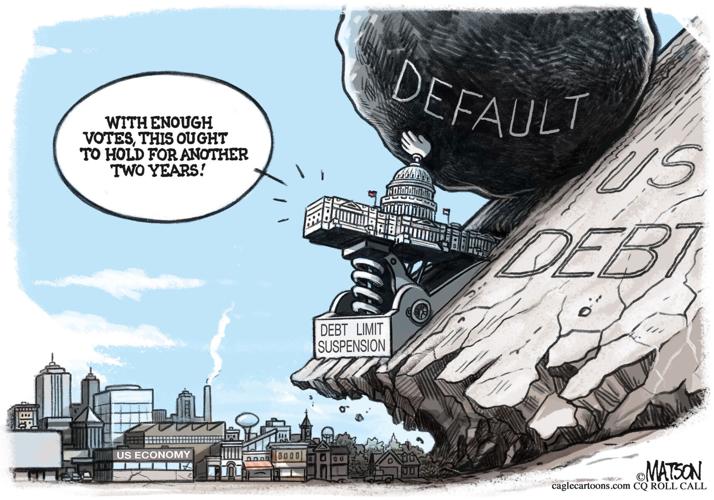

R.J. MATSON: Debt Limit Suspension

- By R.J. MATSON | Syndicated cartoonist

ED WEXLER: McCarthy Doesnt Own The Libs Enough

- ED WEXLER | Syndicated cartoonist

MARSHALL RAMSEY: The Price of Freedom

- By MARSHALL RAMSEY | Mississippi Today

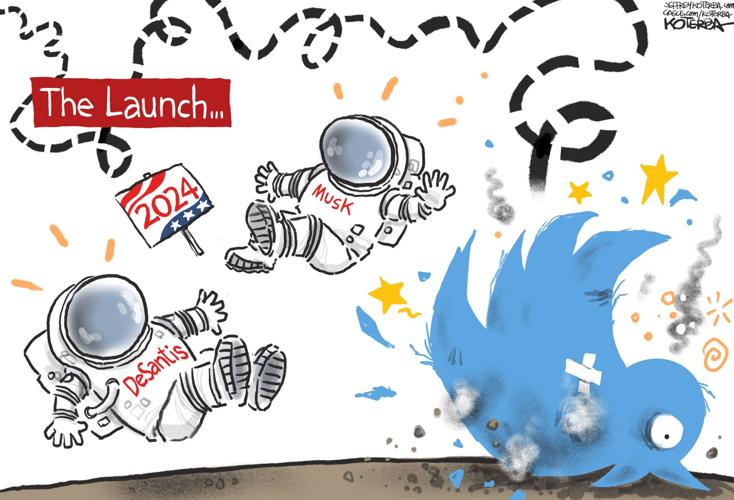

JEFF KOTERBA: DeSantis, Twitter and Musk

- By JEFF KOTERBA | Syndicated cartoonist

JEFF KOTERBA: Tina Turner, Queen of Rock

- By JEFF KOTERBA | Syndicated cartoonist

PAT BAGLEY: Tank Man

- By PAT BAGLEY | Syndicated cartoonist

BOB ENGLEHART: Debt Ceiling Fight

- By BOB ENGLEHART | Syndicated cartoonist

FRANK HANSEN: No Brainer

- By FRANK HANSEN | Syndicated cartoonist

JOHN DARKOW: We Can Police Ourselves

- By JOHN DARKOW | Syndicated cartoonist

GUY PARSONS: Biden vs. McCarthy

- By GUY PARSONS | Syndicated cartoonist

CHRISTOPHER WEYANT: AI Unleashed

- By CHRISTOPHER WEYANT | Syndicated cartoonist

JOHN DARKOW: Debt Ceiling

- By JOHN DARKOW | Syndicated cartoonist

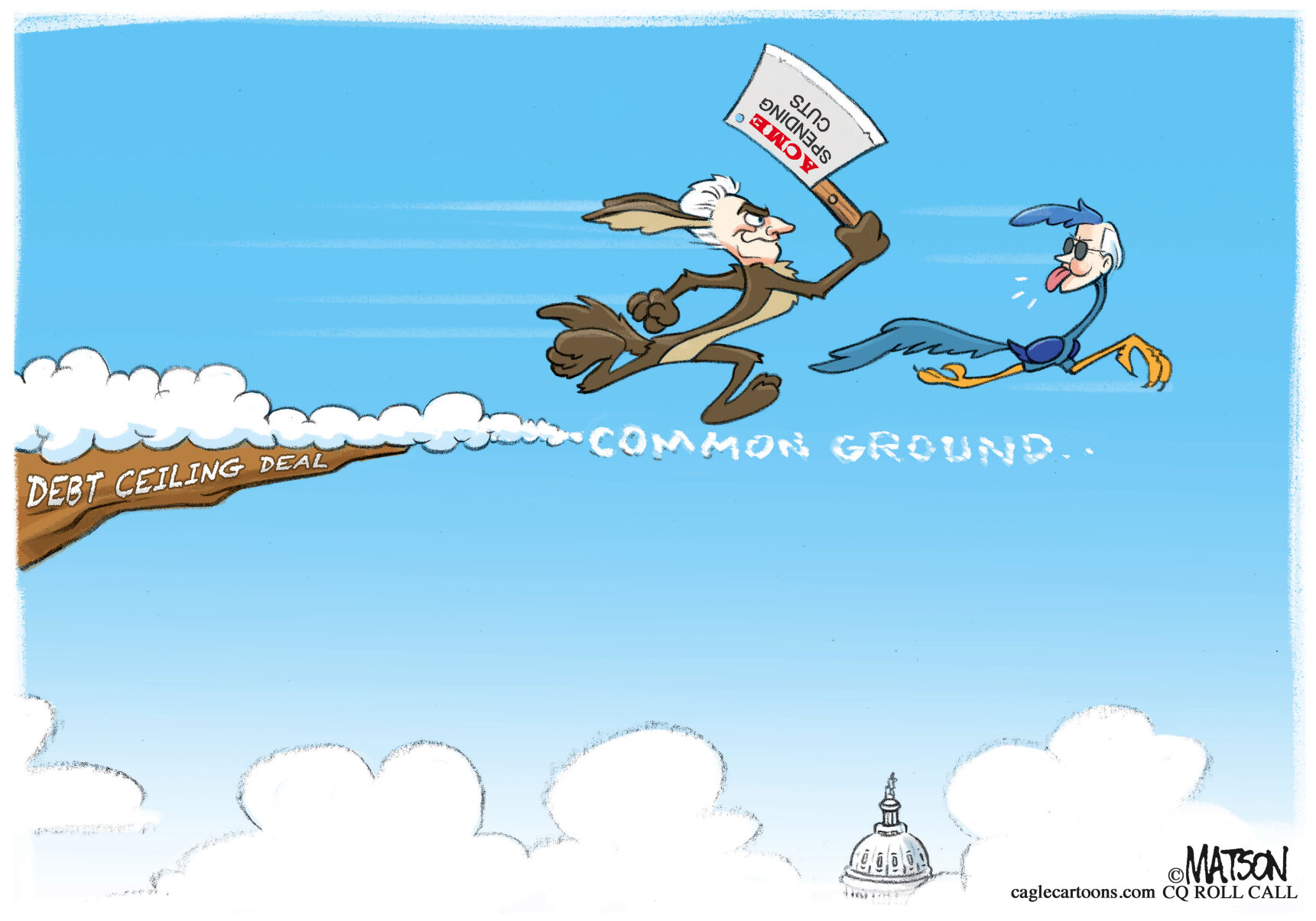

R.J. MATSON: Wile E McCarthy Chases Debt Ceiling Deal

- By R.J. MATSON | Syndicated cartoonist

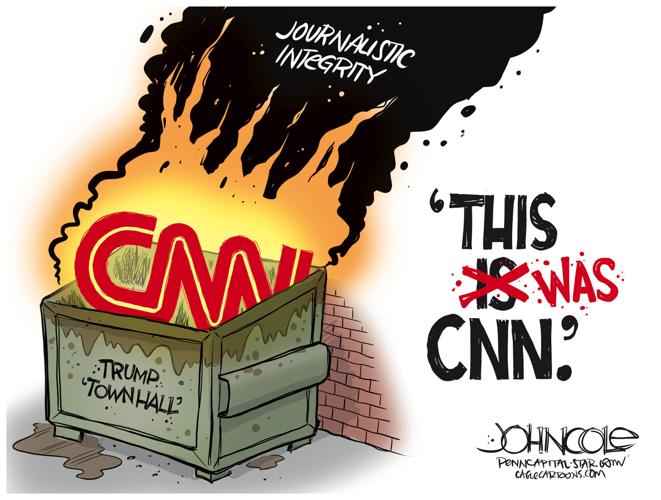

JOHN COLE: CNN's Trump dumpster fire

- By JOHN COLE | Syndicated cartoonist

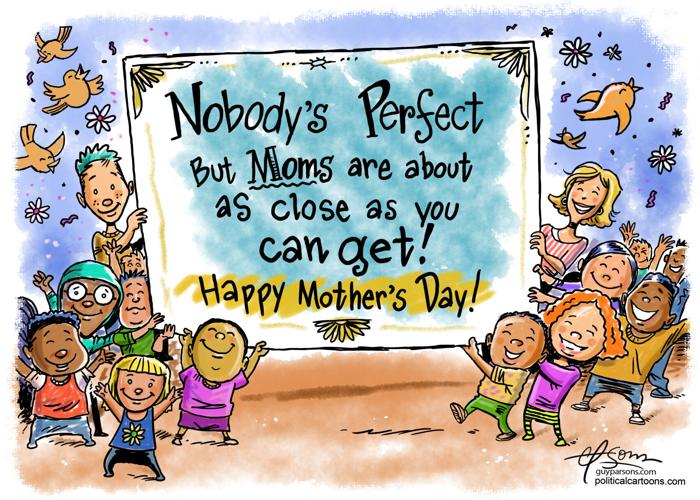

GUY PARSONS: Mom's Day

- By GUY PARSONS | Syndicated cartoonist

ADAM ZYGLIS: CNN Town Hall

- By ADAM ZYGLIS | Syndicated cartoonist

ADAM ZYGLIS: George Santos

- By ADAM ZYGLIS | Syndicated cartoonist

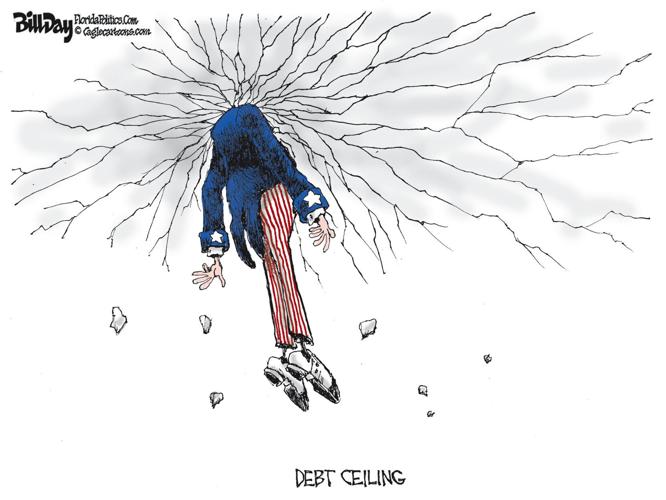

BILL DAY: Debt Ceiling

- By BILL DAY | Syndicated cartoonist

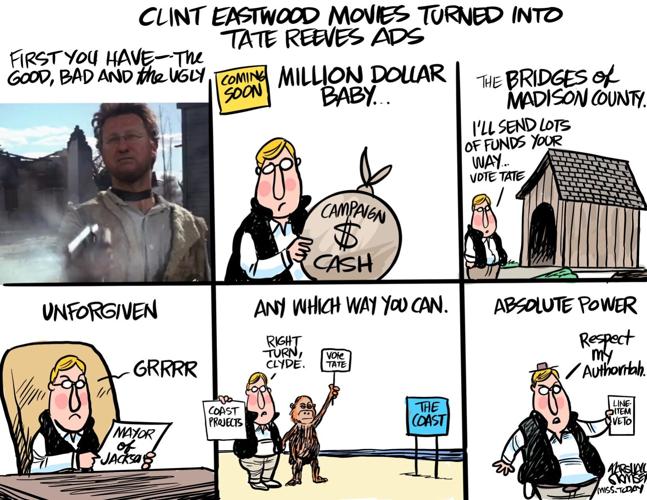

MARSHALL RAMSEY: Clint Eastwood movies in Tate Reeves ads

- By MARSHALL RAMSEY | Mississippi Today

MARSHALL RAMSEY: Tori Bowie

- By MARSHALL RAMSEY | Mississippi Today

DAVE WHAMOND: Supreme Court Justice Trophy

- By DAVE WHAMOND | Syndicated cartoonist

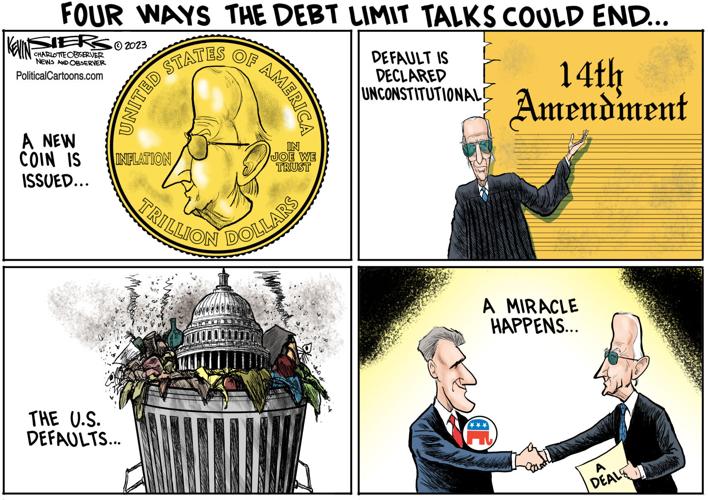

KEVIN SIERS; How the debt limit talks end

- By KEVIN SIERS | Syndicated cartoonist

CHRISTOPHER WEYANT: Heavy Lies The Crown

- By CHRISTOPHER WEYANT | Syndicated cartoonist

DICK WRIGHT: Good Credit Penalized

- By DICK WRIGHT | Syndicated cartoonist

BOB ENGLEHART: Writers Strike

- By BOB ENGLEHART | Syndicated cartoonist

MARSHALL RAMSEY: Tucker's next gig

- By MARSHALL RAMSEY | Mississippi Today

R.J. MATSON: At The Biden Trump 2024 Starting Line

- By R.J. MATSON | Syndicated cartoonist

kAmp44@C5:?8 E@ 42=4F=2E:@?D 3J tG6C4@C6 x$x[ 3FJ6CD H:E9 DEC@?8 4C65:E D4@C6D 36EH66? fa_ 2?5 fbh H9@ >2<6 `dT\a_T 5@H? A2J>6?ED H:== D66 E96:C C2E6D :?4C62D6 3J _]fd_T] q@CC@H6CD H9@ AFE 5@H? a_T\adT H:== D66 C2E6D :?4C62D6 3J _]d__T]k^Am

kAm%96 H:??6CD 2C6 3@CC@H6CD H:E9 H62< 4C65:E D4@C6D — E92E :D[ C:D<:6C 3@CC@H6CD] &?56C 4FCC6?E uwup A@=:4J[ 2 3@CC@H6C H:E9 2 H62< 4C65:E D4@C6 36=@H ea_[ H9@ :D 3@CC@H:?8 >@C6 E92? hdT @7 E96 G2=F6 @7 E96:C 9@>6[ A2JD b]fd_T] &?56C |D] %9@>AD@?’D ?6H A=2?[ E9@D6 3@CC@H6CD H:== D66 E96:C 766D 564C62D6 3J `]fd_T]k^Am

kAm|D] %9@>AD@?[ H9@ C68F=2E6D u2??:6 |26 2?5 uC655:6 |24[ D2JD E96 7656C2= >@CE8286 8F2C2?E@CD “5@?’E DF3D:5:K6 3@CC@H6CD 32D65 @? E96:C 4C65:E D4@C6D]” qFE E96 ?6H uwup ?F>36CD H:== C65F46 766D 7@C 2== 3@CC@H6CD H:E9 4C65:E D4@C6D 36=@H eg_ 2?5 2== 3@CC@H6CD H9@ 92G6 2 5@H? A2J>6?E @7 dT @C =6DD]k^Am

kAm%96D6 ?F>36CD >2EE6C 3642FD6 E9:D :D 9@H E96 >@CE8286 >2C<6E AC:46D C:D<] (96? E96 4@DE @7 =@2?D :D 5:D4@??64E65 7C@> E96 =:<6=:9@@5 @7 5672F=E[ 325 E9:?8D 92AA6?]k^Am

kAm%96 p>6C:42? t?E6CAC:D6 x?DE:EFE6 =@@<65 2E 5672F=E C2E6D @7 u2??:6^uC655:6 @H?6C\@44FA:65 b_\J62C 7:I65 C2E6 AFC492D6 =@2?D 24BF:C65 :? a__e\a__f 2?5 7@F?5 E92E 2>@?8 3@CC@H6CD H:E9 4C65:E D4@C6D 36EH66? fa_ 2?5 feh 2?5 a_T 5@H? A2J>6?ED[ E96 5672F=E C2E6 H2D 36EH66? c]aT 2?5 g]gT] p>@?8 3@CC@H6CD H:E9 =6DD E92? cT 5@H? A2J>6?ED 2?5 4C65:E D4@C6D 36EH66? ea_ 2?5 ebh[ E96 5672F=E C2E6 H2D 36EH66? bh]bT 2?5 de]aT]k^Am

kAm|D] %9@>AD@? D2JD E96 =@2? 766 492?86D H:== DFAA@CE =@H6C\:?4@>6 9@>6 3FJ6CD H9@ “?@?6E96=6DD 92G6 E96 7:?2?4:2= 42A24:EJ 2?5 4C65:EH@CE9:?6DD E@ DFDE2:? 2 >@CE8286]” qFE |D] %9@>AD@? :8?@C6D E92E E96 uwup 92D 2=D@ D=2D965 766D 7@C 3@CC@H6CD H9@ 92G6 D>2== 5@H? A2J>6?ED 2?5 A@@C 4C65:E]k^Am

kAm{@H6C:?8 766D @? 9:896C\C:D< >@CE8286D 5@6D?’E 6?92?46 u2??:6 2?5 uC655:6’D “D276EJ 2?5 D@F?5?6DD]” s:G@C4:?8 AC:46 7C@> C:D< 4C62E6D 5JD7F?4E:@? :? E96 >@CE8286 >2C<6E[ D@>6E:>6D :? F?AC65:4E23=6 H2JD[ 2?5 E2IA2J6CD 2C6 @? E96 9@@<] %96 766D >2J ?@E 6G6? >2<6 9@FD:?8 >@C6 277@C523=6 3642FD6 :?4C62D:?8 56>2?5 H:E9@FE >@C6 DFAA=J H:== C6DF=E :? 9:896C AC:46D]k^Am

kAm%96 CF=6 :D 7:?2==J 86EE:?8 ?@E:465 :? r@?8C6DD[ H9:49 >2J 2=D@ 92G6 |D] %9@>AD@?’D 2EE6?E:@?] w@FD6 u:?2?4:2= $6CG:46D r@>>:EE66 r92:C !2EC:4< |4w6?CJ 2?5 w@FD:?8 2?5 x?DFC2?46 DF34@>>:EE66 r92:C (2CC6? s2G:5D@? D2:5 E96J’== ECJ E@ C6A62= E96 766 492?86D :7 E96J E2<6 67764E 2D A=2??65]k^Am

kAm%96 uwup :D ECJ:?8 E@ >2<6 9@FD:?8 >@C6 277@C523=6 7@C D@>6 3FJ6CD 3J 492C8:?8 @E96CD >@C6] $@F?5D =:<6 D@4:2=:K:?8 4C65:E C:D< E@ FD]k^Am